KiwiSaver is a savings scheme to help you set up for your future. You can spend it when you turn 65, or put it towards purchasing your first home.

Over 3 million people are KiwiSaver members here in Aotearoa New Zealand, so it’s definitely something you might want to learn more about and consider joining sooner rather than later – as you’ll see, there are definite upsides to getting started with a KiwiSaver scheme provider.

How does it work?

When you are a KiwiSaver member a percentage of your wages/salary is automatically deducted from your pay each week, which is then invested in the share market on your behalf.

Which might sound like a bit of a drag – you might have better ideas as to what you could do with that income. But hold off on any judgements yet. The best part about KiwiSaver is that it’s not just you putting money aside for your future each week.

If you’re a New Zealand citizen and working for salary or wages (even if it’s a part-time job), it starts with you deciding how much of your pay to put aside into a KiwiSaver account. It can be between 3% and 10%.

Your employer is then required to also pitch in a minimum contribution of 3% into your KiwiSaver account (if you’re 18 years old and over) – this is in addition to your regular salary/wages. This is called ’employer contributions.’

And then the government also puts money aside for you – as long as you put a minimum of $1,042 per year into your account ($20/week), then the government will pay you $521 each year. This is called the ‘government contribution.’

Free money, what’s not to love about that?!

Do I have to join?

Nope, signing up to KiwiSaver is totally your choice. But we reckon it’s a really smart choice to make for yourself and the security of your future happiness. We’ll explain why as you read on.

Once you join, you can’t opt-out. But we know you won’t regret it. (And if your personal circumstances change where it’s no longer viable for you to keep making your KiwiSaver contributions, then there are ways to put your contributions on hold).

Reason 1 – buying your first home

After three years of being a KiwiSaver member you are eligible to withdraw your KiwiSaver balance and use it towards your first home.

Getting a deposit together for your first home is hard, especially when we’re young and there are lots of more immediate tempting things to spend our hard-earned cash on.

KiwiSaver is like a savings plan that keeps you honest – the money is taken out of your pay before you receive it so you’re never tempted to spend it, and because it goes into a fund you can’t access, it’s a little bit like ‘out of sight out of mind’ – other than the gratification of checking your growing balance of course!

Reason 2 – you’ve turned 65

The main purpose of KiwiSaver is that you have a lump sum of money to have a decent quality of life when you retire. This money is generally used for things like rent, food, fun and travel.

If you retire before the age of 65 you still have to wait until you turn 65 before you can access your KiwiSaver funds.

The main thing to remember is that KiwiSaver is your long-term savings scheme – it’s there in the background, ticking away and growing in the share market without you really having to think about it.

Ok, I’m on board – how do I join KiwiSaver?

There are three options to get started:

1. Automatic enrolment. When you start a new job, you may be automatically enrolled by your employer if you’re between the age of 18-65 years, in a full-time or permanent role, or on a contract for 28 days or more.

2. Ask your employer. If you’re under 18 years, you won’t be automatically enrolled but you can ask your employer to opt-in. You’ll likely need one of your legal guardians (like a parent) to co-sign your account application form.

3. Through a KiwiSaver provider. You can do this whenever you like and means you will have complete control over which provider you use based on things like returns and investment strategies.

For a full list of KiwiSaver providers you can visit ird.govt.nz/kiwisaver.

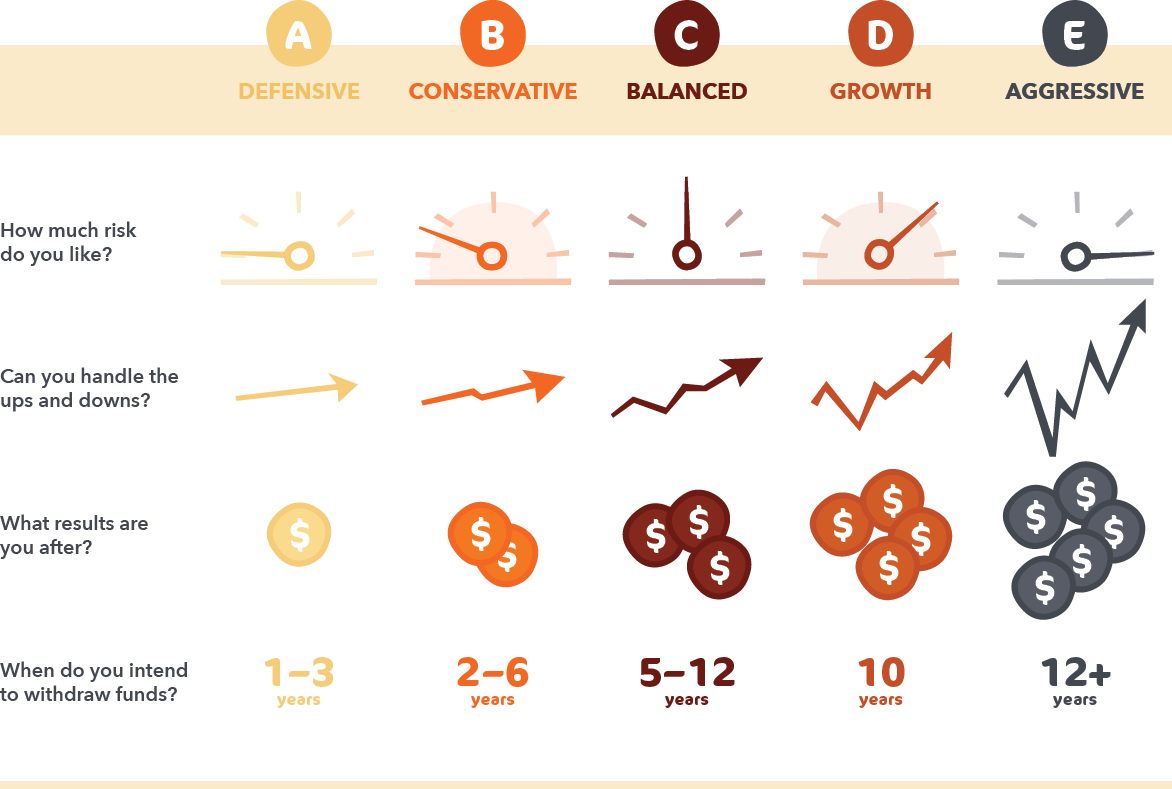

How to choose a KiwiSaver fund

Not only do you get to decide which KiwiSaver provider you will use, but you also have the choice of five different types of funds you want your money invested in.

Which fund you choose comes down to what we call ‘your appetite for risk.’ Are you comfortable seeing your money go up and down and back up again? Or would you prefer to see a steady but slower increase over time?

You might not know which is best for you yet, and that’s ok. You can join us at the Life101 Launchpad to get more direction with your decision-making when it comes to which provider and fund best suits you and your goals, as well as an epic #truthbomb when it comes to the big difference between taking action now or holding off.

We also recommend Inland Revenue’s KiwiSaver guide for young people (click here), and for additional help making your decision about whether to join or not, you can also visit www.sorted.org.nz – it’s the Commission for Financial Capability’s website and provides free, independent information about money matters, including KiwiSaver.

We’re here to help you get a head start on setting yourself up for property ownership and retirement with a breakdown of the ins and outs of joining KiwiSaver, get in touch here with any pātai, or join us over at Launchpad here.